Why Your Auto Insurance Rate Has More to Do With Your Neighbors Than Your Driving Record

The Insurance Math You Never See

You've had a clean driving record for fifteen years, never filed a claim, and drive a safe, reliable car. So why did your insurance premium jump 23% when you moved across town? The answer lies in a complex web of data analysis that has surprisingly little to do with how well you actually drive.

Insurance companies don't just evaluate you — they evaluate your entire neighborhood, your demographic group, and hundreds of factors you'd never associate with auto coverage. Your personal risk profile matters, but it's just one variable in an algorithm that's pricing the probability of claims from people who share your zip code, age, and credit score.

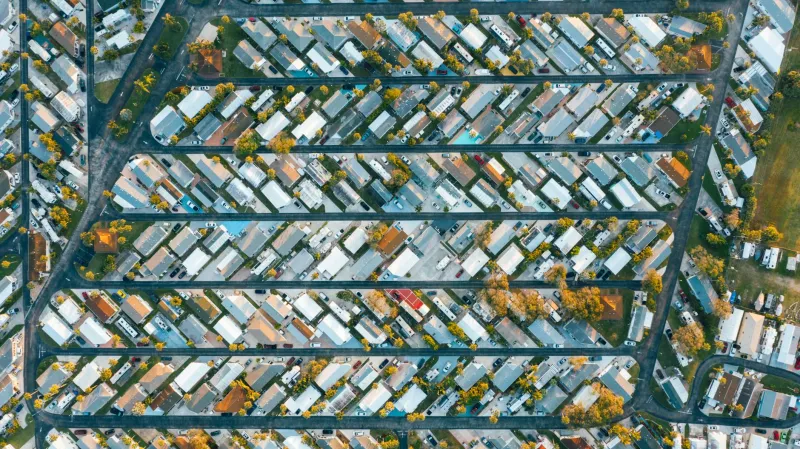

Territorial Rating: Where You Park Determines What You Pay

Every insurance company divides their coverage areas into territories — sometimes as small as a few city blocks. Each territory gets its own base rate calculated from years of claims data from that specific area. Move from one territory to another, and your rate changes even if everything else about your situation stays identical.

These territorial boundaries often make no intuitive sense. Two houses on the same street might fall into different territories with rate differences of 30% or more. The dividing line might be a highway, a school district boundary, or something as arbitrary as a creek that hasn't affected traffic patterns in decades.

Urban areas typically see the most dramatic territorial variations. In Los Angeles, moving from Beverly Hills to certain parts of Hollywood can double your insurance costs. In Chicago, crossing from Lincoln Park into certain nearby neighborhoods can increase premiums by 40%. The risk factors driving these differences include local accident rates, theft statistics, vandalism claims, and even the frequency of uninsured drivers.

Photo: Beverly Hills, via image.r18hub.com

Photo: Beverly Hills, via image.r18hub.com

Photo: Los Angeles, via www.fodors.com

Photo: Los Angeles, via www.fodors.com

The Credit Score Connection Nobody Talks About

In most states, insurance companies use credit-based insurance scores to set premiums. This isn't your regular credit score — it's a specialized algorithm that correlates credit behavior with insurance claims. Studies show that people with lower credit scores file more claims, though the reasons aren't entirely clear.

The correlation is strong enough that credit-based scoring can affect your premium more than a minor traffic violation. Someone with excellent credit and a speeding ticket might pay less than someone with poor credit and a perfect driving record. The insurance industry argues this isn't about income discrimination — they claim it's pure actuarial science based on claims patterns.

Critical life events that damage credit — divorce, medical bankruptcy, job loss — can increase your insurance costs even if they don't affect your driving. The system essentially penalizes financial stress, which often correlates with life circumstances beyond anyone's control.

Population Density Creates Counterintuitive Pricing

You might assume that rural areas with open roads and light traffic would have lower insurance rates than crowded cities. The reality is more complicated. Rural areas often see higher rates due to longer emergency response times, limited medical facilities, and the higher speeds involved in rural accidents.

Meanwhile, some dense urban areas have surprisingly low rates because residents drive fewer miles annually, accidents happen at lower speeds, and there's better access to medical care and vehicle repair facilities. The relationship between population density and insurance costs isn't linear — it's a complex calculation involving dozens of local factors.

How Local Crime Rates Affect Your Car Insurance

Your comprehensive coverage premium is heavily influenced by local property crime statistics, even if you've never had anything stolen. Insurance companies track vehicle theft rates, vandalism claims, and break-in frequency by neighborhood. Areas with higher property crime see significantly higher comprehensive coverage costs.

This creates some strange pricing anomalies. A safe driver living near a area with frequent car break-ins might pay more for comprehensive coverage than someone with a history of at-fault accidents living in a low-crime suburb. Your personal security measures — garage parking, alarm systems, good locks — matter less than the statistical likelihood of claims in your area.

The Weather Factor You Never Consider

Local weather patterns affect insurance pricing in ways most people don't realize. Areas prone to hail storms see higher comprehensive coverage costs. Regions with frequent ice storms have higher collision rates during winter months. Even excessive heat can increase claims due to tire blowouts and cooling system failures.

Insurance companies analyze decades of weather data and claims patterns to build these correlations into their pricing models. Climate change is actually forcing insurers to constantly recalibrate their territorial pricing as weather patterns shift and extreme events become more frequent in areas that historically didn't experience them.

Why Demographics Matter More Than Driving Skills

Age and gender affect insurance pricing, but so do factors like marital status, education level, and occupation. Married people typically pay less than single people with identical driving records. College graduates often get discounts compared to those with high school diplomas. Certain professions — teachers, engineers, scientists — frequently qualify for group discounts.

These demographic factors are based on statistical analysis of claims patterns across millions of policyholders. Insurance companies have found that these life circumstances correlate with driving behavior and claims frequency, even when controlling for other factors.

The Uninsured Driver Problem

Areas with high rates of uninsured drivers see higher premiums for everyone else. When uninsured drivers cause accidents, insured drivers' companies often end up paying through uninsured motorist coverage. These costs get spread across all policyholders in the area.

Some states have uninsured driver rates above 25%, meaning one in four drivers has no coverage. Living in these areas increases everyone else's premiums significantly, regardless of individual driving records or personal responsibility.

How Local Infrastructure Affects Your Rate

Road quality, traffic light timing, highway design, and even street lighting influence accident rates and insurance costs. Areas with poorly designed intersections, inadequate road maintenance, or confusing traffic patterns generate more claims.

Insurance companies track which specific intersections, highway ramps, and road segments generate the most claims. Living or commuting near accident-prone infrastructure can increase your rates even if you're personally a careful driver who's never had an accident there.

The Medical Cost Connection

Local medical costs significantly affect personal injury protection and bodily injury liability premiums. Areas with expensive hospitals and medical specialists see higher insurance rates because the cost of treating accident victims is higher.

This creates geographic disparities that have nothing to do with driving risk. A minor accident in Miami might generate $15,000 in medical bills, while the same accident in rural Kansas might cost $4,000. Insurance premiums reflect these local cost differences.

What Actually Moves Your Rate

While you can't control your zip code's claims history or local crime rates, understanding these factors helps explain rate changes and shopping strategies. Moving to a different territory within the same city can sometimes save hundreds of dollars annually. Shopping around becomes more important in high-cost territories because companies weight these factors differently.

Your driving record still matters, but it's just one input in a complex calculation that includes dozens of factors beyond your control. The insurance industry isn't necessarily trying to be unfair — they're trying to predict risk based on patterns in massive datasets. The result is a system where your neighbors' behavior often matters as much as your own.